By Erica Wenham, Thursday 17 May 2013.

Modern Marketing Information & Analysis (Week 28 - Exam Revision)

“Danone Activia: How a little bit of T.L.C.

made a market leader”

Principal Authors: Rowenna Prest and Alice Huntley,

RKCR/Y&R

Contributing Authors: Alan Bloodworth and Benjamin Morgan,

OHAL; Beatrice Boue, MEC; Shawn Pitt, Millward Brown

(Institute

of Practitioners in Advertising/IPA)

Silver, IPA

Effectiveness Awards, 2012

Introduction

This is a story of how a challenger brand became leader in

an especially competitive market. How a brand built on a functional claim to be

the solution to a particular kind of problem found a way to engage an even

wider group of consumers who didn't identify with that problem. How a small pot

of yoghurt gave over 10 million people a simple way to give themselves a little

bit of T.L.C. How a new brand platform delivered incremental sales of £58.6

million, a net profit of £3.6 million and an ROI of 23%. This is the story of

Activia.

Activia to 2009

The Activia brand is part of

the Chilled Yogurts & Desserts (CYD) market which by 2009 was worth over

£2.2billion. This category is tough, dominated by high-spending brands. And as

a discretionary part of the shopping basket, constant streams of new products

are launched, competing to keep consumers interested. Activia grew

exponentially in value from 16th in 2004 to 2nd by 2007. There it stayed vying with, but never

overtaking, the market leader Müller Corner.

Activia’s Ambition for 2010

In 2010, Activia UK had to be a true talisman for success:

being 2nd wasn't

good enough. In 2010 the brand’s agency were tasked to make Activia number 1.

To achieve this, Activia needed to grow faster than Müller Corner, which meant

they had to grow their value by 7%, equating to over £13 million value sales.

What Communications Had To

Do

Activia is a strong product

with a high repeat purchase rate: in 2009 70% who bought Activia did so more

than once (Fig. 1). Once hooked, the frequency of purchase is high: 6.6/year

versus 4.6/year for Müller Corner.

Fig. 1: Repeat purchase rate for Activia

in 2009

As a result, the company knew

trial would deliver more growth than frequency of purchase amongst an already

loyal customer base. To meet the 2010 target of 7% value growth Activia needed

to increase household penetration by 3.5 points to 38%, in other words add

900,000 new consumers.

The Challenges

Yogurt is a healthy category,

and Activia had a health claim: being a solution to the problem of

"digestive disorders". This refers to a broad set of self-reported

issues which the Activia U&A study demonstrated were experienced by 57.7%

of women.

By December 2009, household

penetration of Activia was 34.5%, two-thirds of whom (i.e. the 21% segment in

Fig. 2) reported digestive disorders.

Fig. 2: UK female Activia user & non-users,

split by those who do and don't suffer from digestive disorders (Source:

Activia U&A, TNS, June 2008. Base: 610 women aged 18 to 70 years old,

nationally representative)

But why hadn't this 36.7% tried it already?

The top three barriers to purchase amongst this potential

group were relevance, price, and taste (Fig. 3):

Fig. 3: Top 3 barriers to trial

amongst non-users with digestive disorders (Source:

Activia U&A, TNS, June 2008. Base: 224 women aged 18 to 70 years old, who

have a digestive disorder but don't use Activia)

Barrier 1:

Lack of Relevance

Lack

of relevance amongst people with digestive disorders seemed peculiar. Activia

had been successfully marketed on the basis of a widespread problem, so people

with that problem should be open to trying it.

Qualitative

research showed that however convincing their consumer testimonials had been

for many, there were many others who, who even if they said they sometimes

experienced the symptoms on the U&A survey, didn't think they had a

digestive "problem". Simply, it wasn't for them, it was for 'others'.

- "I just don't suffer from that bloated

stomach thing and that's what those ads say"

- "I've seen that ad before and I thought it

looked really good, but it isn't for me because I don't have that

problem."

- "It doesn't interest me one iota because I

don't have that bloated thing"

(Source: IPSOS, May 2008)

Looking at frequency of suffering of digestive disorder

revealed two-thirds didn't experience them often enough to feel they had a

problem (Fig. 4).

Fig. 4: Frequency women claimed to

suffer from digestive (Source:

Activia U&A, TNS, June 2008. Base: 352 women aged 18 to 70 years old, who

have a digestive disorder)

It

was clear that to continue increasing penetration Activia needed an idea that

would move beyond the "problem" and make the benefit of Activia more

relevant to more women.

However,

Activia were mindful that broadening relevance couldn't be at the expense of

differentiation. BrandAsset Valuator, (which measures brand perceptions,

linking them to commercial performance), demonstrated both were important to

build brand strength and a market leading position (Fig. 5).

Fig. 5: BAV Powergrid In 2008 Activia

had to increase relevance & differentiation (Source: BAV, Y&R UK. Base 1,856 British

women, nationally representative)

Barrier 2:

Price

Activia

was sold at a premium. The business felt confident that if they could fix

relevance and taste perceptions, price would cease to be a barrier, proved by

the high repeat purchase rate amongst existing users.

Barrier 3:

Taste

Taste

was an essential driver in the category.

"Health looks set to remain on the nation's long-term food

agenda, but taste is still the top factor in consumers' choice of snacks.

Against these often contradictory demands facing snacks, the majority view of

yogurt as a healthy but tasty snack and a popular alternative to chocolate or

desserts puts it in a rare, strong position for long-term growth."

(Source: Kiti Soininen, Senior Food

Analyst, Mintel)

Fortunately, Activia was very tasty.

Users see Activia's taste as even more of a benefit than its

ability to reduce bloating, impacting more on its repeat purchase rate. But for

non-users, the problem of bloating obscured taste, leading to low taste

expectations. (Fig. 6)

Fig. 6: Unprompted benefits of

Activia: users vs. non-users (Source:

Activia U&A, TNS, June 2008. Base: 610 women aged 18 to 70 years old,

nationally representative)

Whilst

Activia's positioning had to centre on health, as this is where the equity of

the brand had been built, they needed a positioning flexible enough to address

all three barriers.

Solving

the Challenge

Their hunch, backed up by the findings of the IPA, was that a

broader, more emotional health positioning would be more powerful. Activia commissioned

research to see what would happen if the brand were to be re-positioned:

Fig. 7: Hypothesis on how Activia's

positioning ought to shift (Source:

RKCR)

The results discovered the following:

Talking about a happy tummy was a more

positive way to reference Activia's benefit and delivered

a rich emotional territory

Results

surprisingly showed how much potential users had to say about their tummies. A

healthy tummy didn't just mean you didn't have to linger in the loo; it meant

you felt great too, inside and out.

- "If you are healthy you are happier"

- "When your tummy is right you feel better,

more confident, better able to tackle things"

- "When your tummy is working you are

happy"

(Source: Cre8tive Research, Nov 2008)

The bigger emotional need was for a bit

of T.L.C., not just a remedy for tummies

The

mums spoken to were facing endless and exhausting multitasking, resulting in

little time to care for themselves:

- "We're usually bottom of the pile"

- "I care much more about my husband or

children's insides than mine"

(Source: Cre8tive Research, Nov 2008)

As a result, the brand and agency felt confident that Activia

could play a role in helping the nation's mums look after themselves; helping

them have happy tummies and making them feel good on the inside and outside.

The Brand New Idea

The

organisation used these insights to create a powerful brand platform, which

positioned Activia as a delicious champion of happy tummies everywhere.

The

creative idea was to hijack the common term "T.L.C.", imbuing it with

new meaning, no longer "tender loving care", but "tummy loving

care."

Research

showed this idea had the potential to resonate powerfully with women;

- "It pricks your

conscience that you should think about yourself more"

- "It made me feel better - because it's moved

me away from the bloated thing"

- "It's quite caring and warm in a way"

- "People will remember T.L.C. - tummy loving

care"

(Source: Cre8tive Research, Nov 2008)

Importantly,

given the competitive nature of the market, it still felt distinctive- no other

brand owned this emotional territory.

A clear communications

strategy was now put into place (Fig. 8):

Fig. 8: Activia's 2010 Communications

Strategy (Source: RKCR)

A

New Communications Approach

1) Creative Vehicle

Championing Women's Right to T.L.C.

Activia

wanted to motivate women that they had the right to a little T.L.C, a much

bigger message than normally delivered by CYD brands. So, communications had to

have a confident, upbeat, almost celebratory in tone to convey the sense of

feeling great.

Activia

developed a positive rallying cry to the women of Britain to love their

tummies, with the phrase 'Give yourself some Tummy Loving Care', underpinned by the rousing classic, Gimme Some Lovin".

Delivered by an Engaging, yet Identifiable Champion

Finding

the right person to champion this cause was key.

It's

been well documented that the use of a celebrity, if done well, can

significantly increase engagement.

Activia needed someone who a), women could

relate to and b), might credibly need a little help to keep their tummies on

track.

Countless

celebs failed to make the cut.

Then

they struck gold.

Activia

found the nation's typical 'girl next door': Martine McCutcheon.

Her

appeal was strong, having starred in big heart of the nation entertainment such

as Eastenders and Love Actually. Yet, in spite of her success, research found

that the target audience could still identify with her:

"I like Martine

McCutcheon she is a real woman - not all skin and bone like some."

"You can imagine her shopping in Tesco's like we do."

Source: Movement, T.L.C. Creative

Development, 2008

Looking like a

Market Leader

Activia wanted to feel like a

brand for everyone. But also wanted Activia to feel like a leader, building an

iconic image in consumers' minds. So, they developed a strong visual for

Activia T.L.C. (Fig. 9 & 10) which ran as posters, a media rarely used by

other CYD brands.

Fig. 9: Activia launch poster &

key visual

This

image was then successfully taken across other media, such as the Activia

website (Fig. 10)

Fig. 10: Activia’s website with key

visual

2)

Media & Messaging

Delivering Taste: The Flexibility of the Creative Thought

and Vehicle

The

testimonial approach made delivering non-health messages difficult. However,

because 'T.L.C was a clear idea with more flex, it could carry a range of

messages, including taste. After all, as the previous quote indicated people

believed Martine wouldn't be shy indulging her taste buds.

Market-Leading

Media Behaviour (Econometrics)

Activia acted like

a market leader, increasing its media investment by 17% and share-of-voice by 8% (Fig. 11)

Source: MEC&OHAL

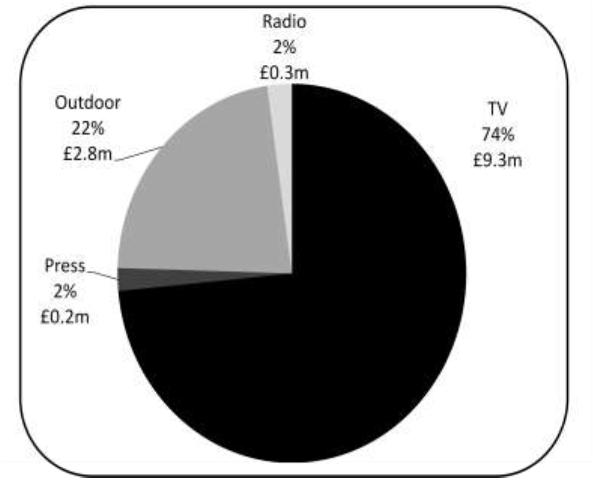

TV predominantly delivered this (Fig. 12) because it was

excellent at provoking an emotional response and econometrics had proved its

ability to payback for Activia previously. Outdoor was the key secondary media,

delivering the brand stature worthy of a market leader.

Fig. 12: Activia's media 2010

spend/channel (Source: MEC)

Media

placements built relevance. TV was placed in key 'talkable' slots and strong

daytime programming. Posters were placed where busy women were most likely to

be i.e. train stations, bus stops and in proximity to supermarkets.

Maximising the Relevance of T.L.C.

Activia

were confident we had a strong, engaging creative vehicle and were working off

a strong insight which would deliver the necessary relevance to a broader audience.

However,

we knew we could increase relevance further by launching the campaign at a time

when more tummies were gurgling for T.L.C, and when women were most likely to

be considering their future health and happiness... New Year

This

contextual insight was confirmed by research;

- "I always think,

new year, new start"

- "By New Year I'm thinking about sorting

myself out"

(Source: Movement TLC Creative

Development Research, 2008)

So

New Year was when Activia launched T.L.C. (Fig. 13)

Fig 13: Activia

TLC Launch

Example of creative flexibility (Fig. 14), delivering a

variant and taste message.

Fig. 14: Activia Intensely Creamy

(variant & taste)

By

Summer 2010, Activia had successfully overtaken Müller Corner. Acting as market

leader, we encouraged consumers to make this the 'Summer of T.L.C and were

confident enough to make great taste our lead message.

Summary

of Comms Approach

Fig. 15: Activia's 2010 Communications

Approach (Source: RKCR)

Business

Results

The brand’s agency had been tasked to grow Activia to number

one in market. Activia needed to achieve a minimum value growth of 7%, worth an incremental £13m, by driving

penetration 3.5 points to 38%, equating to 900k new customers.

After the launch of the T.L.C. campaign penetration significantly

increased (Fig. 16).

Fig. 16: Activia's household

penetration vs. actual TVRs in 6 month increments (Source: AC Nielsen, April 2009-January

2011, 52wk rolling data; MEC actual TVRs. (Note: Activia only buy data for the

past 3 years which is why a 12 month pre comparison wasn't able to be made))

A

more granular look (Fig. 17) shows that Activia met the 38% target 2 months

ahead of plan, finishing the year a point ahead, attracting 1.2 million new

customers (versus 900k target).

Fig. 17: Activia's household penetration vs. actual

TVRs (Source: AC Nielsen,

April 2009-January 2011, 52wk rolling data; MEC actual TVRs.)

As

a result, value sales (Fig. 18) also saw a significant rise:

Fig. 18: Activia's total market value

sales (4 weekly rolling)

(Source: AC Nielsen, April 2009-January

2011. (There is a seasonality factor to the CYD market. Due to only being able

to get 3 years data we can't show all of 2009 vs. 2010. However, the Christmas

dip in 2010 is still £1.65million higher than in 2010.))

Activia

beat its 7% increase in value sales target by 1.9 points, delivering

incremental sales of £20.1 million, (£7.1m above target). Müller Corner

performed less strongly than expected, but even if it had grown at its

2008-2009 rate, Activia would have still edged ahead (Fig. 19).

Fig. 19: 2009 vs. 2010 Value Sales (Source: Nielsen)

The

increase in value sales meant Activia increased its value share by 7% whereas Müller Corner

remained static; this enabled it to take its position as market leader (Fig. 20)

Fig. 20: Value Share of Chilled Yogurt

& Dessert Market 2009 vs. 2010 (Source:

Nielsen)

Activia's

growth outperformed the market, even though it grew by 1.7%, instead of a

projected 1%. (Fig. 21)

Fig. 21: CYD Value Sales 2009 vs. 2010 (Source:

Nielsen)

Summary of Business Results

Fig. 21b: Summary of Activia's 2010

business results (Source: Nielsen

& RKCR)

The

Impact of Advertising

Activia have demonstrated a step-change in penetration and

value growth concurrent with the launch of T.L.C. They then proceeded to prove

that advertising was the key driver of this change by:

- Demonstrating

that advertising worked as intended

- Using

econometric modelling from OHAL to precisely identify the contribution of

advertising

Activia and their

marketing/advertising agency also underwent the exercise of eliminating other

factors using a range of sources. However, OHAL's model has an R2 of 99% which proves all significant factors have been

accounted for.

The advertising has worked as intended

Activia successfully changed

the behaviour of over 1.2 million UK consumers, but had communications

made the attitudinal shifts identified?

For advertising to have made

these shifts, it had to be noticed. Brand tracking demonstrated that Activia's

communications awareness increased by 28% over 2010 (Fig. 22).

Fig. 22: The % Women who were aware of

Activia advertising December 2009 vs. January 2011 (Source: Millward Brown. Base 320 women.

Statistically significant to 95% confidence level.)

The

media efficiency (spend/awareness) increased slightly Y-O-Y (Fig. 29) which

suggests the increase wasn't solely down to spend.

Fig. 23: Media efficiency 2009 vs.

2010 (Source: Millward Brown

& MEC)

Whereas

the previous testimonial campaign struggled to engage consumers, the T.L.C.

campaign had no problem, performing 29% better. (Fig. 24)

Fig. 24: Average Activia Engagement

Score 2009 vs. 2010 (Source:

Millward Brown. Base 320 women.)

Engagement

and awareness of T.L.C. helped drive relevance by 26%. (Fig. 25)

Fig. 25: The %

Women who agreed, 'Activia is for people like you December 2009 vs. January 2011 (Source:

Millward Brown. Base 320 women. Statistically significant to 95% confidence

level.)

Perceptions

that Activia maintained digestive health also increased (Fig. 26).

Fig. 26: The % Women who agreed,

'Activia helps maintain digestive health', December 2009 vs. January 2011 (Source:

Millward Brown. Base 320 women. Statistically significant to 85% confidence

level)

Taste

perceptions improved by 8% (Fig. 27).

Fig. 27: The % Women who agreed, 'Activia is great tasting' December 2009 vs. January 2011 (Source:

Millward Brown. Base 320 women. Statistically significant to 85% confidence

level)

A

key aim of the campaign had been to increase the number of women who'd consider

giving themselves some T.L.C. Consideration over the period increased by 27%

(Fig. 28).

Fig. 28: The % Women who agreed, 'I

would consider Activia December 2009 vs.

January 2011 (Source: Millward

Brown. Base 320 women. Statistically significant to 95% confidence level.)

In

summary, all attitudinal measures improved over the T.L.C. campaign period:

Fig. 29: Summary of attitudinal shifts

towards Activia (Source: Millward

Brown & RKCR)

Penetration

increase is the best proof of actual trial but claimed trial also increased,

with an uplift of 17% (Fig 30):

Fig. 30: The % Women who agreed, 7 have tried Activia' December 2009 vs.

January 2011 (Source: Millward

Brown. Base 320 women. Statistically significant to 95% confidence level.)

The Shift in Relevance

made Activia increasingly perceived as a Market Leader

Significant

improvement in relevance is corroborated by BAV.

Due

to the survey's scale it's not run every year but data from 2008 vs. 2011 is

available which provides a good indicator of campaign impact.

It

shows Activia grew from 64.2nd ranked percentile to the impressive 80.4th percentile out of 1,500 brands. Importantly, broadening

relevance wasn't at the cost of distinctiveness, which grew to the 86.1st percentile (Fig. 37), making Activia in the top 20% of all UK

brands on these measures. Impressive for a lowly yogurt pot.

Fig. 31: How UK female perceptions

have shifted across 4 key brand health measures (Source: Y&R UK. Base 1,856 women in

2008, 815 women in 2011. Statistically significant to 99% confidence. Note due

to the sale of study it isn't run every year but the 2008-2011 time frame gives

Activia an idea of perception shifts during the campaign.)

This growth meant Activia had strongly consolidated its

position in people's minds as market leader (Fig. 32)

Fig. 32: BAV Power Grid showing,

Activia increasing in market-leader perceptions (Source: Y&R UK. Base 1,856 women in

2008, 815 women in 2011.)

This

put Activia ahead of many other well known FMCG brands, many of which were now

considered mass market rather than market leading, and in the company of 'super

brands' such as Apple, Dyson and Coca-Cola. It also put Activia ahead of Müller

Corner. (Fig. 33)

Fig. 33: Perceptions of Activia vs.

other market leaders (Source: Y&R UK. Base

1,856 women in 2008, 815 women in 2011.)

This

consolidation as market-leader is important because the Powergrid relates to

future financial growth (Fig. 34). 'Leadership' brands have a much higher projected

growth versus 'mass market'.

Fig. 34: Multiple of intangible value

per unit sale (Source: Y&R)

Econometrics

Econometric modelling has been used

to identify and accurately quantify the effect of advertising and other

relevant factors on Activia's sales.

The fit of the model is very strong

with an R2 of >99%.

OHAL have supplied us with the

incremental uplift figures which take into account the full impact of

advertising. It looks at the campaign period, but also includes the longer term

impact of the advertising with a cut off period of 52 weeks.

The model demonstrates that the 2010

T.L.C. campaign drove an incremental uplift of £58.6million revenue from sales

of Activia.

Confidentiality prevents Activia from

publishing actual gross profit. So, as in the previous 2008 IPA paper, the

brand’s researchers have used an average margin for this category as a proxy to

help us establish whether the advertising was profitable for Danone. OHAL's

experience in this category indicates that it is reasonable to assume a gross

profit margin of 33% which gives us an incremental profit of £19.5million.

Minus the total marketing cost

(production, media spend and agency fees) of £15.9million, the end campaign had

generated £3.6 million incremental profit.

So, for every pound spent,

advertising generated a profit of £1.23 (Fig. 35).

Fig. 35: TLC's 2010 Return on

Marketing Investment (Source:

OHAL & RKCR)

Conclusions

& Wider Learnings

1)

Market leaders differentiate themselves

both emotionally and functionally

This

case shows how it's possible to develop powerful emotional platforms that

resonate widely with consumers, but still retain the functional product truth

that is at the heart of a brand's original differentiation. For Activia, this

ensured a solid platform for continued growth and market leadership. As the

client commented,

"Launching the T.L.C. campaign successfully ensured Activia's

position as market leader and gave us a great platform to build from for the

future" - Corinne Chant, Marketing Director of Danone UK.

2)

Behaving like a leader can make you a

leader

Activia

were ambitious enough to go for No.1 slot, and brave enough to move on from a

highly successful but ultimately limiting functional communications approach.

Like a leader they adopted a more emotional platform, and they supported that

platform with the media investment and behaviour of a leader.

3)

Driving trial with new users is a

powerful engine of growth for high quality products

When

you know you have a product that performs very well for people, sometimes all

you have to do is overcome the barriers that prevent new people trying it.